- Catalogs

- Fincantieri - Cantieri Navali Italiani

- PRESENTATIONS 1.4

- Products

- Catalogs

- News & Trends

- Exhibitions

PRESENTATIONS 1.4

PRESENTATIONS 1.4

- Revenues rose by 1.3% compared to 1H 2016, with an EBITDA margin increase to 6.3% from 5.0%.

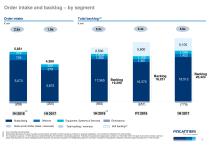

- Total backlog reached €25.5 billion, covering approximately 5.8 years of work based on 2016 revenues.

- Backlog increased to €20.4 billion, with a soft backlog of €5.1 billion.

- Delivered five units, including three cruise ships and two naval vessels.

- VARD's diversification strategy is progressing, leveraging synergies with the cruise business.

- Acquired 66.66% of STX France's share capital, pending conditions and negotiations with the French State.

- Significant orders include 12 cruise ships and various vessels for different clients.

- Main deliveries include cruise ships "Silver Muse," "Viking Sky," and "Majestic Princess."

- Shipbuilding: Growth in cruise revenues, with 22 vessels in backlog and deliveries scheduled up to 2027.

- Offshore: Production volumes reduced due to downturns, but diversification strategies are in place.

- Equipment, Systems & Services: Revenue decline due to lower ship conversion activities.

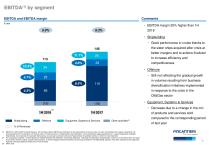

- EBITDA margin improved by 20% compared to 1H 2016.

- Net result before extraordinary items improved, with increased finance expenses due to foreign exchange impacts.

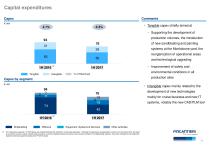

- Capital expenditures focused on production volume development and technological upgrades.

- Net working capital decreased to €206 million, reflecting cruise production growth.

- Construction loans increased, typical of the cruise business financial flows.

- Shipbuilding: Expected growth in volume and margin due to higher-priced cruise sister ships and the Italian Navy’s fleet renewal program.

- Offshore: Anticipated volume growth due to Vard's diversification strategy, despite potential impacts from the Oil & Gas sector crisis.

- Equipment, Systems & Services: Significant backlog deployment related to the Italian Navy’s fleet renewal program and focus on core products and after-sales development.

- 2018 Guidance: Revenue increase of 16-23% compared to 2016, EBITDA margin of approximately 6-7%, and net debt of approximately €0.4-0.6 billion.

- 2020 Guidance: Revenue increase of 16-21% compared to 2018, EBITDA margin of approximately 7-8%, and net debt of approximately €0.1-0.3 billion.

- Shipbuilding: Revenues increased by 9.9% to €1,757 million, with a 6.5% EBITDA margin. Orders decreased to €3,872 million from €5,073 million in 1H 2016. The backlog increased to €18,512 million.

- Offshore: Revenues decreased by 16.4% to €448 million, with a 4.8% EBITDA margin. Orders decreased to €379 million from €729 million in 1H 2016. The backlog increased to €1,403 million.

- Equipment, Systems and Services: Revenues decreased by 11.3% to €227 million, with an 11.1% EBITDA margin. Orders slightly increased to €323 million from €318 million in 1H 2016. The backlog increased to €1,288 million.

Catalog excerpts

Safe Harbor Statement This Presentation contains certain forward-looking statements. Forward-looking statements concern future circumstances and results and other statements that are not historical facts, sometimes identified by the words "believes," "expects," "predicts," "intends," "projects," "plans," "estimates," "aims," "foresees," "anticipates," "targets," and similar expressions. The forward-looking statements contained in this Presentation, including assumptions, opinions and views of the Company or cited from third party sources, are solely opinions and forecasts reflecting current views...

Open the catalog to page 2

(1) Sum of backlog and soft backlog FinCAnTIERI (2) Soft backlog which represents the value of existing contract options and letters of intent as well as contracts in advanced negotiation, none of which yet reflected in the order backlog ~ i, ^ - h

Open the catalog to page 3

1H 2017 main orders Orders acquired in Q2 Norwegian Cruise Line Holland America Line (Carnival Corporation) 1 krill fishing vessel Aker BioMarine 1 live fish transportation vessel Fjordlaks Aqua 1 research expedition vessel Rosellinis Four-10 2020 (wholly-owned by the industrialist Kjell Inge Røkke)

Open the catalog to page 4

Cruise ship “Viking Sky” Cruise ship “Majestic Princess” Cruise ship “Silver Muse” FREMM “Rizzo” Submarine “Romeo Romei” OSCV “Skandi Buzios” OSCV “Far Superior” OSCV “Skandi Vinland” Client Viking Ocean Cruises Princess Cruises (Carnival Corporation) Silversea Cruises Italian Navy Italian Navy Techdof Farstad DOF Deliveries in Q2 Delivery Ancona Monfalcone Sestri Ponente Muggiano Muggiano Vard Soviknes Vard Vung Tau Vard Langsten

Open the catalog to page 5

(1) Sum of backlog and soft backlog (2) Soft backlog represents the value of existing contract options and letters of intent as well as contracts in advanced negotiation, none of which yet reflected in the order backlog (3) For comparison purposes, 1H 2016 figures are restated following the redefinition of operating segments. Following the operational reorganization carried out in November 2016, the repair & conversion services, cabins & public areas business, as well as integrated systems business, all previously included in the Shipbuilding segment, have been relocated to the Equipment, Systems...

Open the catalog to page 6

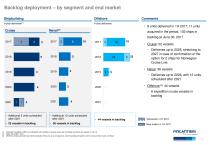

Backlog deployment – by segment and end market Shipbuilding # ship # ship deliveries • 8 units delivered in 1H 2017, 11 units acquired in the period, 102 ships in backlog at June 30, 2017 − Deliveries up to 2025, stretching to 2027 in case of confirmation of the option for 2 ships for Norwegian Cruise Line • Naval: 36 vessels − Deliveries up to 2026, with 12 units scheduled after 2021 • Offshore(3): 44 vessels − 6 expedition cruise vessels in backlog • Additional 5 units scheduled after 2021 • 22 vessels in backlog (1) (2) (3) • Additional 12 units scheduled after 2021 Articulated Tug Barge (ATB)...

Open the catalog to page 7

Breakdown by segment and end market^ Shipbuilding - Growth of revenues in cruise, reaching 51% of Group’s total (3 units delivered and 11 units under construction vs. 4 units delivered and 9 units under construction in 1H 2016) Offshore - Reduction of production volumes due to the downturn in production activities in European shipyards of VARD, pending the contribution of the diversification strategy - Shut down of Niteroi yard in Brazil - Positive effect of NOK/EUR exchange rate (€ 11 mln) Equipment, Systems and Services - The decline in revenues is mainly due to a lower contribution from ship conversion...

Open the catalog to page 8

EBITDA and EBITDA margin € mln Shipbuilding Offshore Equipment, Systems & Services Other activities3 Comments • EBITDA margin 20% higher than 1H 2016 • Shipbuilding - Good performance in cruise thanks to the sister ships acquired after crisis at better margins and to actions finalized to increase efficiency and competitiveness • Offshore - Still not reflecting the gradual growth in volumes resulting from business diversification initiatives implemented in response to the crisis in the Oil&Gas sector • Equipment, Systems & Services - Decrease due to a change in the mix of products and...

Open the catalog to page 9

Net result before extraordinary and non recurring items^ € mln • The result before extraordinary and non recurring items reflects Attributable to owners of the parent Attributable to non-controlling interests (1) Excluding extraordinary and non recurring items net of tax effect - Improvement of operating performance and margin - Increase finance expenses at € 39 mln (vs € 32 mln in 1H 2016), due to the reduction of unrealized foreign exchange gains for € 15 mln related to a Vard Promar loan in Brazil (vs. income of € 19 mln in 1H 2016) • Extraordinary and non recurring items gross of tax effect...

Open the catalog to page 10

Comments • Tangible capex chiefly aimed at - Supporting the development of production volumes, the introduction of new sandblasting and painting systems at the Monfalcone yard, the reorganization of operational areas and technological upgrading - Improvement of safety and environmental conditions in all production sites • Intangible capex mainly related to the development of new technologies mainly for cruise business and new IT systems, notably the new CAD/PLM tool Shipbuilding Offshore Equipment, Systems & Services Other activities <1) For comparison purposes, 1H 2016 figures are restated...

Open the catalog to page 11

Breakdown by main components Comments € mln FY 2016 1H 2017 Inventories and advances to suppliers Work in progress net of advances from customers Trade receivables Other current assets and liabilities Construction loans Trade payables Provisions for risks & charges Construction loans are committed working capital financing facilities, treated as part of Net working capital, not in Net financial position, as they are not general purpose loans and can be a source of financing only in connection with ship contracts Net working capital decrease to € 206 mln, from € 265 mln in FY 2016 Increase of...

Open the catalog to page 12All Fincantieri - Cantieri Navali Italiani catalogs and brochures

COSTA FIRENZE

COSTA FIRENZE2 Pages

SILVER MOON

SILVER MOON2 Pages

ENCHANTED PRINCESS

ENCHANTED PRINCESS2 Pages

Submarine U212A Todaro Class

Submarine U212A Todaro Class2 Pages

SEVEN SEAS SPLENDOR

SEVEN SEAS SPLENDOR2 Pages

VIKING JUPITER

VIKING JUPITER2 Pages

CARNIVAL HORIZON

CARNIVAL HORIZON2 Pages

CARNIVAL PANORAMA

CARNIVAL PANORAMA2 Pages

NIEUW AMSTERDAM

NIEUW AMSTERDAM2 Pages

SKY PRINCESS

SKY PRINCESS2 Pages

2018 FULL YEAR RESULTS

2018 FULL YEAR RESULTS25 Pages

KONINGSDAM

KONINGSDAM2 Pages

CARIBBEAN PRINCESS

CARIBBEAN PRINCESS2 Pages

Archived catalogs

RUBY PRINCESS

RUBY PRINCESS2 Pages

REGAL PRINCESS

REGAL PRINCESS2 Pages

MAJESTIC PRINCESS

MAJESTIC PRINCESS2 Pages

passenger ferry

passenger ferry2 Pages

F.-A.-Gauthier

F.-A.-Gauthier2 Pages

Inshore Patrol Vessels

Inshore Patrol Vessels2 Pages

Offshore Patrol Vessels

Offshore Patrol Vessels2 Pages

FINCANTIERI

FINCANTIERI50 Pages

ANNUAL REPORT 2016

ANNUAL REPORT 2016140 Pages

Business Plan 2016-2020

Business Plan 2016-202015 Pages

Transverse Tunnel

Transverse Tunnel6 Pages

M 10-16

M 10-162 Pages

PRESENTATIONS

PRESENTATIONS14 Pages

Company Profile

Company Profile74 Pages